MHRA’s Point‑of‑Care Manufacturing Framework

The UK’s MHRA unveils first-of-its-kind framework allowing hospitals to manufacture personalized cell and gene therapies on-site.

A New Era for Cell & Gene Therapy

Just last week, the UK Medicines and Healthcare products Regulatory Agency (MHRA) quietly did something revolutionary: it switched the regulatory focus for advanced therapies from where they are made to how their quality is controlled. The Human Medicines (Amendment) (Modular Manufacture and Point of Care) Regulations 2025 create the first dedicated legal pathway that allows hospitals, and even mobile clean‑room units, to complete the final stages of cell‑ and gene‑therapy manufacture right at the patient’s bedside.

What the new rules actually say

The legislation introduces two new manufacturing licenses. A Manufacturer’s License (Point of Care) covers fixed hospital suites, while a Manufacturer’s License (Modular Manufacture) captures relocatable or mobile micro‑factories. In both cases a single control site (e.g. a centre of excellence or a technology provider) holds the license, maintains the quality‑management system and supervises every distributed site in real time through a master file. The framework applies not only to autologous CAR‑T and gene‑edited cell products but also to 3‑D‑printed implants, medicinal gases and a handful of other short‑shelf‑life products that have previously struggled to fit into the conventional GMP regime.

Crucially, the MHRA has also tightened historic exemptions that allowed clinicians to skirt full GMP by talking about “simple mixing at the bedside.” If you are performing anything that looks like manufacture e.g. cell expansion, genome editing, final formulation, aseptic fill, you now need to follow the new license route. In return the field gains regulatory recognition that some therapies cannot survive a cross‑country drive to a central facility, let alone an international flight.

Why therapeutic developers should take notice

For developers of cell and gene therapies the POC framework is more than an administrative tweak. In fact, it reshapes CMC, clinical development and launch strategy in one move. Processes that were previously split between a primary facility and a courier can now be divided between a central hub for complex manipulations and a hospital suite for the high‑risk, time‑critical finishing steps. That change alone can shave days off vein‑to‑vein time, reduce cryo‑shipping failures and unlock adaptive trial designs that rely on immediate dosing.

Regulatory‑CMC teams will need to engage early with the MHRA to agree the contents of the POC Master File, the location of batch‑release testing and the digital systems that underpin real‑time oversight. The agency has signaled a willingness to use its Innovative Licensing and Access Pathway (ILAP) to accelerate such conversations, but developers should expect probing questions about data integrity and remote intervention protocols.

Commercial leaders, meanwhile, must rethink launch footprints. A therapy that can be finished on‑site will naturally gravitate toward NHS trusts with established GMP capacity, shifting the centre of gravity away from a single national facility toward a federation of hospital networks. Intellectual‑property management also rises up the agenda: closed, automated systems, secure SOPs and encrypted audit trails become proprietary assets that differentiate one therapy from another.

Implications for the enabling‑technology ecosystem

If you build the tools that power advanced‑therapy manufacture, the UK has just become an essential proving ground. Hospitals will seek compact, closed, automated suites that can drop into existing infrastructure without a multi‑million‑pound refurbishment. Those systems must stream batch data back to the control site, plug directly into electronic batch records and trigger remote release testing that takes hours rather than days.

Software providers face parallel opportunities and responsibilities. The distributed model only works if every site can be seen, in real time, by the license holder and, by extension, the MHRA. Expect hospitals to demand digital twins, inline analytics and AI‑assisted deviation handling as standard, not as premium add‑ons. Rapid microbial sterility tests, single‑use bioreactors optimized for autologous volumes, and augmented‑reality training modules will all find a readier market now that the regulatory path is clear.

Go‑to‑market strategy should also shift. NHS trusts, not just biotechs, become primary customers. Vendors that can wrap hardware and software into a turnkey, compliance‑by‑design offering will have a compelling first‑mover advantage. Success in the UK will provide a template that other regulators are likely to emulate, turning early adoption into global leverage.

The Lonrú perspective: clients navigating first and fast

At Lonrú we see three immediate priorities. First, therapeutic developers should map their existing manufacturing architecture and pinpoint which unit operations could be safely migrated to a point‑of‑care environment. Second, both developers and tool providers should initiate early scientific‑advice dialogues with the MHRA to clarify expectations around digital quality management, remote batch release and control‑site governance. Finally, stakeholders must invest in robust tech‑transfer packages, complete with remote‑support protocols and tamper‑proof data pipelines since the distributed model is only as strong as its weakest node.

The UK has opened the door to a future in which genuinely personalized medicines can be made, tested and delivered within the same clinical encounter. Those who step through early will help define the standards the rest of the world adopts and will gain invaluable operational insight and skills along the way. Lonrú Consulting stands ready to guide developers and technology providers alike through this new landscape, from strategy and competitor landscaping to hospital‑channel execution.

Beyond NPV: Quantifying Patient Benefit in Cell & Gene Therapies

Picture an investment committee reviewing two first-in-class gene-editing programs. Financial models show identical risk-adjusted NPVs, yet one promises four times the projected patient benefit. Which wins the vote? The story isn’t about any single foundation; it’s about a recurring dilemma in CGT financing where dollars and patient impact don’t always point to the same deal.

Traditional rNPV remains the lingua franca of venture finance, but CGT’s high R&D costs, small patient pools and curative ambitions make monetary returns unusually volatile. Layering patient impact alongside NPV offers a stabilising compass, ensuring capital flows toward programmes that move both the balance-sheet and the survival curve. Just last week, Philip Brainin (Associate at Sound Bioventures) published a new framework in Nature Biotechnology to measure the societal impact of venture investments in life sciences.

Quick Primer on SALYs & SADYs

Brainin’s framework proposes two patient-centric metrics tailored for investors. Science-Adjusted Life Years (SALYs) and Science-Adjusted Disability Years (SADYs) building on global health metrics like DALYs and QALYs but adjust for:

Probability of Scientific Success: SALYs are discounted by the likelihood a therapeutic candidate clears regulatory hurdles.

Equity Ownership: SALYs can be normalized per $ invested, per share class, or per co-investor share creating comparability across venture and public-private deals.

Where DALYs account for disease burden lost, SALYs forecast life-years gained a new measure grounded in both biology and market realism. SALYs and SADYs incorporate four key elements: (i) disease incidence, (ii) target-product-profile reach, (iii) change in likelihood-of-approval, and (iv) survival or disability benefit into a single number that discounts for scientific risk while scaling for real epidemiology.

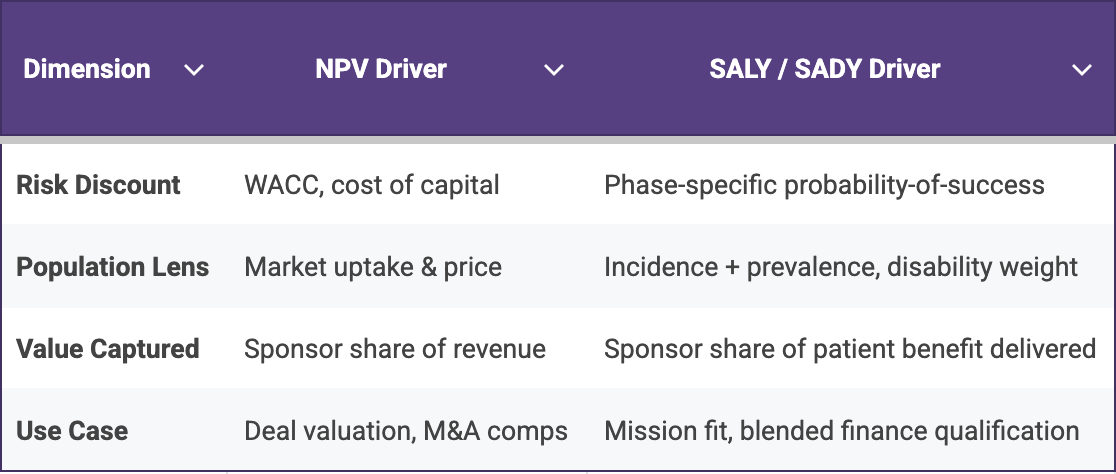

NPV reaches first for finance levers: discount rates, price and market uptake, while the SALY/SADY construct substitutes phase-specific probabilities of success, incidence and disability weights. The side-by-side comparison in Table 1 below makes the contrast explicit and underscores why the two metrics work best together: NPV flags capital efficiency, while SALY/SADY illuminates the magnitude of patient impact.

Table 1. Financial levers dominate NPV calculations, whereas disease burden and probability estimates dominate SALY/SADY making the two metrics complementary rather than redundant.

Cell and Gene Therapies: The Ultimate Stress-Test

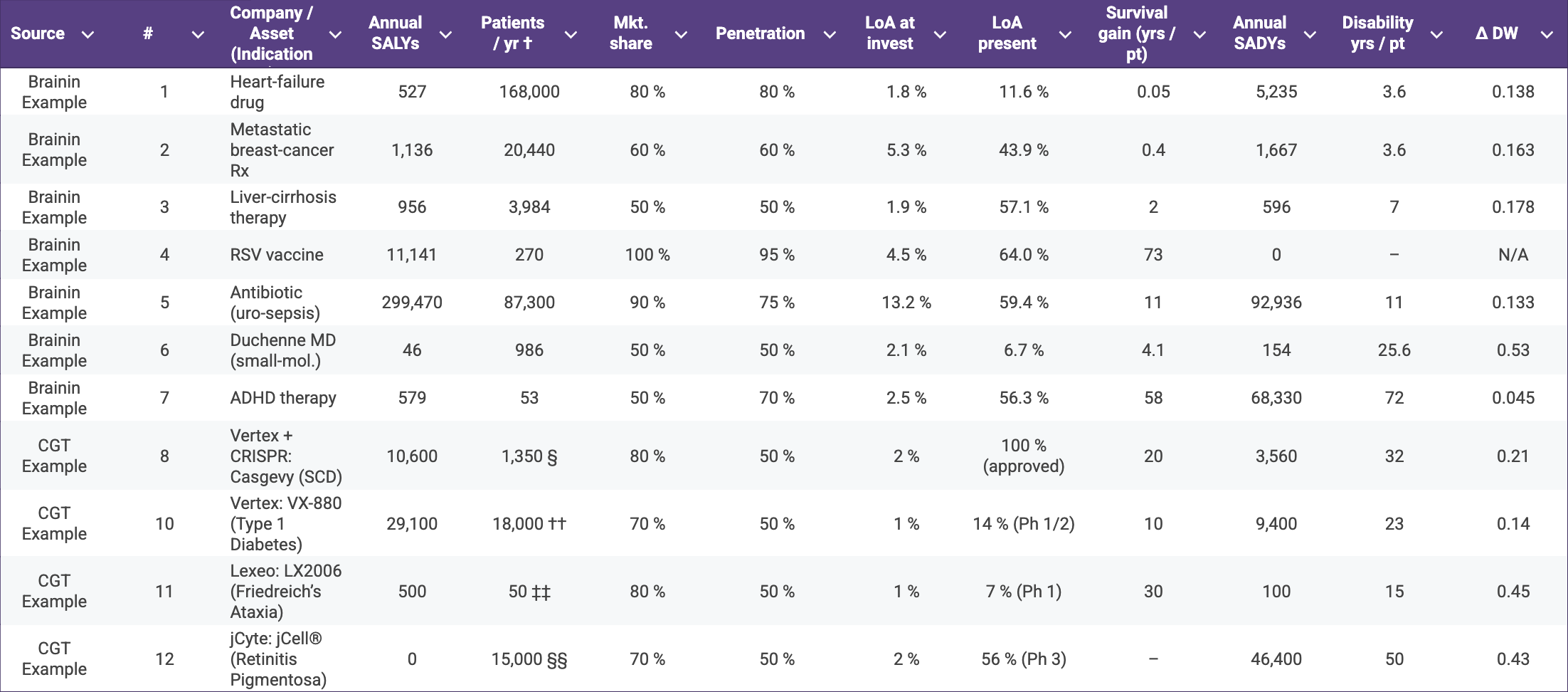

Because single-dose curative therapies concentrate an entire lifetime of revenue into an upfront payment, traditional rNPV estimates can fluctuate sharply with every adjustment to price assumptions. In contrast, SALYs ground the analysis in quantified patient benefit, providing a more stable indicator of programme value. For example, a one-time prime-editing treatment targeting just 400 patients may still generate several thousand discounted SALYs, demonstrating substantial societal impact even when the commercial total addressable market remains modest. That analysis may be crucial for foundations deciding between grants and equity, as well as HTA agencies assessing early economic value and impact funds seeking to prove additionality.

The matrix below illustrates how SALY and SADY calculations can re-rank programmes once patient-benefit intensity is considered. High-incidence mainstream drugs (e.g., an antibiotic for urosepsis) unsurprisingly dominate absolute SALY totals, yet several CGT examples; Casgevy for sickle-cell disease, Vertex’s VX-880 for type 1 diabetes, and Lexeo’s LX2006 for Friedreich’s ataxia deliver double- and triple-digit SALY counts from comparatively smaller patient pools.

Table 2. Annual Science-Adjusted Life-Years (SALYs) and Science-Adjusted Disability-Years (SADYs) for representative therapeutics spanning Brainin’s original examples and a selection of cell- and gene-therapy (CGT) assets†

† Incident U.S. patient population, mirroring Brainin’s convention.

§ Birth prevalence ≈ 1 : 2,024 (CDC) → ~1,830 births / yr; halving to those with ≥ 2 VOCs ⇒ 1,350.

¶ U.S. annual DMD diagnoses estimated at 300–400 boys / yr (1 : 5 000 male births).

†† CDC reports just over 18,000 youth diagnosed with T1D each year.

‡‡ FA affects 1/50,000 people; 4 M births × 1/50,000 ⇒ ~80 births; 60 % meet cardiac-gene-therapy criteria ⇒ ~50.

§§ GenSight estimates 15,000–20,000 new RP vision-loss cases per year in the US + EU; mid-point used for US.

Value for Patient Alliances & Impact Investors

The comparison highlights why impact-minded investors, foundations, and HTA agencies should weigh both population size and per-patient life-year gain rather than relying on rNPV alone: a modest-TAM curative can still generate a disproportionate share of risk-adjusted patient benefit. Moreover, quantified patient benefit can arm advocates with data for accelerated review petitions, outcome-based pricing arguments and R&D tax-credit campaigns.

Inserting SALY forecasts into horizon-scans lets bodies like NICE or FDA’s Health-Equity initiative flag high-impact indications earlier. Likewise, manufacturing grants, fee waivers or voucher tweaks can be recalibrated to favour high-SALY but commercially challenging diseases.

Implementation Playbook

Lonrú’s VantagePoint™ Suite can combine global burden of disease epidemiology with our proprietary phase-transition probability library to generate turnkey SALY/SADY dashboards. Beyond the analytics, Lonrú can partner directly with patient alliances to run evidence-gathering workshops, analyse and validate disability weights, and co-author advocacy briefs that translate SALY insights into concrete asks for regulators and payers. Lonrú Consulting operates as a neutral translator between financial, clinical and patient voices. By integrating Brainin’s novel SALY/SADY calculus into our advisory workflows, we can help stakeholders steer capital and policy toward truly transformative CGT programmes.

Bridging The Data Gap On The Pediatric CRISPR Highway

Reflections On The new CZI-IGI Centre for Pediatric CRISPR Cures

(Follow-up to our previous post “Building the U.S. Interventional-Genetics Interstate”)

Last week, the Chan Zuckerberg Initiative (CZI) and the Innovative Genomics Institute (IGI) unveiled a $20 million Center for Pediatric CRISPR Cures that will treat eight children using bespoke gene-editing protocols and share data and methodology with other academic centres, amplifying the impact to reach more patients. The funding cements a highway-scale build-out of personalised editing that began with Baby KJ’s bespoke therapy announced earlier this year. Below we zoom in on KJ’s blueprint, note the opportunities that remain for tools and service providers, focusing on the not yet mentioned data-infrastructure lane. And we’ll discuss how rapidly growing Databricks and Snowflake solutions could slot in beside the big-cloud contenders.

KJ’s blueprint was tuned to target the liver, requiring a liver-specific off-target panel, and relied on six-to-eight-week reagent lead-times and notably had no disclosed informatics backbone. Those gaps are build-out opportunities to accelerate the next phase: ligand-decorated or capsid-mimetic nanoparticles for bone-marrow / CNS delivery, bench-top mRNA/gRNA micro-factories with “factory-as-code” manufacturing systems, duplex long-read safety assays folded straight into IND templates, and overlaying it all, a federated data layer able to convert patient record streams into Beacon-discovery and real-world-evidence dashboards at interstate speeds informing the next patient-specific therapy.

Figure 1: Blueprint of the “next-gen” CRISPR-cure highway: from patient intake, through rapid design and micro-factory production, into a secure cloud backbone that feeds real-world evidence back to the very first node.

Who might “pour the concrete” for the missing data layer?

The heavy lifting will almost certainly happen on one of the big public-cloud platforms - it’s just a question of which one provides the right plug and play solutions.

Amazon Web Services already offers a specialist toolbox called AWS HealthOmics. Think of it as a ready-made workshop where research centres can upload genetic data and run standard pipelines without building their own servers. It even hosts an open-source workflow standard called GA4GH-WES (basically a universal “power outlet” for genomic software).

Google Cloud brings its Healthcare API which acts like a data-ingestion gate built around the hospital record format FHIR, plus BigQuery, a powerful spreadsheet-on-steroids that analysts love. Google has even published point-and-click guides for translating FHIR data into the research-friendly OMOP layout, so you don’t need an army of data engineers to get started.

Oracle is pitching Oracle Health Data Intelligence, a cloud warehouse that isn’t tied to any one electronic-health-record system but still has hooks into its own Cerner software. Recent upgrades add in-house artificial-intelligence services so users can, for example, predict which patients might respond to a treatment.

Whichever cloud supports the center, the infrastructure will still benefit from specialist “add-ons” to make day-to-day work easy for scientists and compliance officers:

Databricks Lakehouse which operates like a giant notebook for data crunching and can sit near the hospital edge. Teams can write code to clean raw files (that’s the “code-first ETL” piece), build machine-learning models, and then share polished tables using a no-copy hand-off called Delta Share.

Snowflake Healthcare & Life Sciences Data Cloud can act as the central hangar. It provides locked-down “clean rooms” where regulators or insurance companies can analyse data without ever downloading it which is ideal for privacy-sensitive real-world-evidence studies.

Databricks accelerates how quickly each site can generate validated data and scalable models for future custom therapies; Snowflake governs how broadly those insights can be shared and queried. That tandem; fast edge processing plus a secure, elastic core is what turns eight bespoke therapies in CZI/IGI’s center into hundreds of “recipe-ready” cures across multiple hospitals without rebuilding the stack each time. In practice, we could anticipate an “edge Databricks, core Snowflake” pattern: hospitals do their raw prep in Databricks, push the curated results into Snowflake, and Snowflake becomes the official registry - no matter whether the underlying cloud hardware belongs to AWS, Google, or Oracle.

What to watch for next

IGI is expected to disclose the eight-patient disease roster at ASGCT 2026; that list will reveal whether the liver-first foundation can stretch to immune or CNS targets. An RFP for a Beacon v2-compliant registry will tip the favourite cloud stack, and early FDA CBER pilots on distributed CMC will determine how quickly the cookbook and recipes can propagate between hospitals. Vendors that align their delivery tech, analytics panels or micro-factory kits with the eventual backbone will find themselves moving quickly along the newly established gene editing interstate highway, while slower movers will fight for on-ramps.

Who Follows Verve?

Cash Runway, Indication “White-Space”, and Where the Tools Ecosystem Can Play A Part

Lilly-Verve: A Wake-Up Call for the Gene-Editing Supply Chain

Eli Lilly’s agreement to acquire Verve Therapeutics for $1.3 billion delivered the first big-pharma endorsement of an in-vivo base-editing therapy aimed at a common cardiovascular risk factor. For developers this affirms that a well-differentiated programme can command a premium while still in early clinical stages; for the companies that supply lipids, vectors, analytical assays, single-cell QC or GMP processes the message is equally clear: the strategic value of an editing platform now rises or falls with the maturity of its tool-chain. In other words, big-pharma is prepared to pay early only when it can see a credible route to scale-up, and that route is paved by the specialist providers working behind the scenes.

Who We’re Tracking, and Why a Few Familiar Names Don’t Appear

Our lens concentrates on Beam Therapeutics, Intellia Therapeutics, CRISPR Therapeutics, Editas Medicine, Caribou Biosciences, Prime Medicine and Precision BioSciences. Each of these seven companies is publicly listed, still independent, and already has at least one drug-editing programme in the clinic or cleared for first-in-human testing. Recently purchased firms such as Capstan (now inside AbbVie), EsoBiotec (acquired by AstraZeneca) and Poseida (absorbed by Roche) no longer control their own financing cadence, while delivery-only or RNA-editing specialists like ReCode, ShapeTX and Korro tend to measure progress by platform milestones rather than therapeutic read-outs. Note, Precision’s ARCUS technology earns its place even though it is derived from a homing endonuclease rather than Cas9: it performs the same sequence-specific cut in an in-vivo setting and therefore competes for exactly the same opportunities.

White-Space Shots vs. Second-Wave Plays: The Current Indication Map

Within that group the spectrum of ambition is striking. Verve, now partnered with Lilly, and CRISPR Therapeutics are pushing into cardiovascular lipid disorders where no first-generation genome editor has yet secured approval, while Intellia is offering a one-and-done alternative to the chronic RNA-interference treatments already in play for ATTR amyloidosis. Intellia also reported fresh NTLA-2002 data yesterday, boosting investor sentiment but not altering its runway guidance. Programmes from Beam, Editas and Caribou focus on haemoglobinopathies or oncology indications that regulators have already seen in an autologous or first-wave CRISPR guise, making differentiation a question of efficiency, safety and patient access. Prime Medicine and Precision BioSciences step into ultra-rare chronic granulomatous disease and chronic hepatitis B respectively, both areas without an existing curative option. We have added Verve/Lilly to the indication table so we can compare how the acquired asset fits alongside the still-independent cohort.

Source: Lonrú Consulting’s VantagePoint™ analysis, July 2025. The post-Verve field of clinical-stage gene-editors and where each sits on the white space v second wave spectrum.

Charting runway next to market size, and why Verve serves as a useful benchmark

Mapping each company’s publicly guided cash runway on one axis and the projected 2030 market size of its lead indication on the other helps reveal who may seek partnership cash soonest and who can afford to take a longer view on tool selection. The Verve/Lilly transaction provides a helpful reference point: Verve entered the deal with roughly twenty-four months of runway remaining and was addressing a market comfortably north of twenty-five billion dollars. Any company that shows a shorter runway or a smaller commercial opportunity may need to demonstrate an even tighter command of its supply chain, or else invite partnership earlier than planned. For tool providers this plot highlights two complementary paths: larger-TAM, longer-runway players can commit to multi-year, higher-margin supply agreements, whereas shorter-runway firms may look for creative cost-sharing structures that still ensure uninterrupted development.

Source: Lonrú Consulting’s VantagePoint™ analysis (July 2025). Cash-runway figures drawn from latest SEC filings; 2030 market sizes from consensus analyst and disease-area forecasts.

From the supplier’s perspective the priorities differ by modality. In-vivo cardio and hepatitis programmes rely on ever finer lipid chemistry, capsid engineering and genome-wide off-target analytics; vendors that can package those capabilities together become attractive long-term partners. Ex-vivo haem-onc projects remain sensitive to cost of goods and therefore reward vendors who can combine closed-system cell hardware with lean vector manufacture or cost effective alternatives. Throughout, the tone is shifting from transactional reagent sales to collaborative co-development aimed at building IND-ready modules that regulators will recognise.

Signals to Watch and Practical Moves for Lonrú Clients

Regulators are already signalling an interest in longer durability and safety read-outs for single-shot LDL-C and HBV cures, a change that is likely to boost demand for high-resolution sequencing assays and longitudinal biomarker platforms. Macroeconomic uncertainty means companies holding less than eighteen months of cash could accelerate partnering or M&A conversations, potentially redrawing the competitive field in a matter of quarters. Meanwhile, any early clinical success from prime editing or ARCUS could reshuffle licensing appetites in much the same way Verve’s early cardio data did in 2024.

For Lonrú’s clients the immediate takeaway is to align commercial efforts with those scientific and financial inflection points. Cardiometabolic and hepatitis programmes offer the largest revenue head-room and will tolerate premium pricing if the tools accelerate path-to-market, whereas the haem-onc field will reward solutions that deliver efficiency and regulatory clarity at a competitive cost. Engaging earlier; ideally before a cash-short biotech reaches its fund-raising cliff, creates room for more balanced, longer-term collaboration that can survive the inevitable shifts that follow a strategic acquisition.

From Pipeline Fillers to Platform Plays

Yesterday morning, AbbVie dropped a $2.1 billion headline - announcing it will buy Capstan Therapeutics and, with it, a pre-clinical in-vivo CAR-T “toolkit” capable of re-programming immune cells inside the body. The deal isn’t about slotting a single late-stage asset into AbbVie’s post-Humira pipeline; it’s about owning the full technology operating system comprising Capstan’s targeted LNP delivery and its programmable mRNA payloads when combined can spin out dozens of future programs.

Yesterday’s news is the latest, and loudest, data-point in a year-long pattern: Lilly’s base-editing buyout of Verve, BMS’s prime-editing pact with Prime Medicine, and now AbbVie’s Capstan swoop all signal that Big Pharma’s shopping cart has moved from finished goods to modular tech stacks. In this Lonrú Lens post, we’ll unpack why platform control is eclipsing asset acquisition, how in-vivo versus ex-vivo strategies are reshaping CMC and analytics demands, and, most importantly, what this shift means for companies supplying the “picks and shovels” of cell-and-gene-therapy (CGT) manufacturing and quality. Expect a deep dive into the new M&A economics, the tooling gaps Big Pharma just inherited, and the strategic plays that CGT enablers should make before the next billion-dollar platform changes hands.

Why the pivot?

Patent-cliff paranoia: With blockbusters like Humira already off-patent, acquirers are chasing engines that can feed multiple franchises, not one-shot drugs.

CapEx vs Build-time: Buying a fully formed editing or delivery “OS” leap-frogs the 5-7 year slog of internal development.

Competitive moats shift upstream: If editing fidelity, delivery tropism or CMC automation become the differentiators, owning the platform locks competitors out of entire modality classes.

What a platform deal looks like in practice

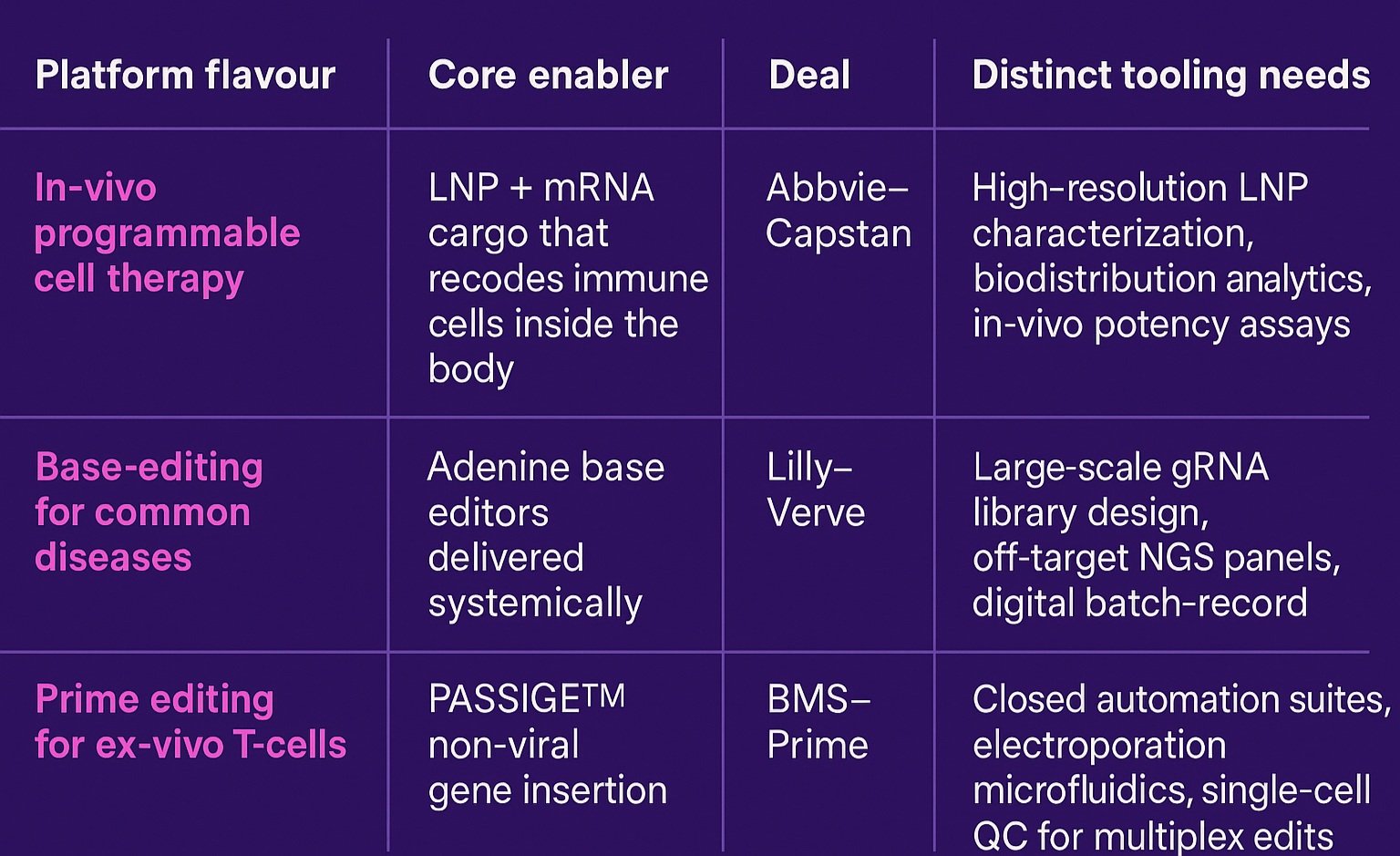

The three deals in focus that have re-framed 2024-25 M&A illustrate just how differently “platform” can look in practice, and why the supporting tool chain must be equally diverse. AbbVie’s buy-in to Capstan gives it an in-vivo programmable-cell platform, where targeted lipid-nanoparticle (LNP) composition and real-time bio-distribution analytics are the gatekeepers of potency and safety. Lilly’s takeover of Verve centres on systemic base-editing, a population-scale play that makes high-throughput gRNA library design, on/off-target NGS panels and seamless digital batch-records non-negotiable. Bristol Myers Squibb’s alliance with Prime Medicine, meanwhile, is rooted in ex-vivo prime editing, pushing the need for closed, automated cell engineering suites and single-cell QC to handle multiplex edits at commercial scale. Read together, the deals prove that Big Pharma isn’t just buying optionality; it’s inheriting distinct, capital-intensive tooling gaps. In the next section we explore how specialised CGT vendors can turn those gaps into growth.

One size doesn’t fit all: each CGT platform archetype carries its own toolbox.

The ripple-effect for CGT tool providers

For companies that make the “picks and shovels” of cell-and-gene manufacturing, the new platform land-grab translates into a race for capacity, data fluency and regulatory credibility, simultaneously. Big Pharma’s acquisition teams have bought themselves ambitious editing blueprints, but they did not buy the supply-chain depth, digital infrastructure or quality modules needed to run those blueprints at scale. That shortfall thrusts specialised vendors into a more strategic role: LNP-analytics firms are being invited to embed directly into CMC work-streams; cloud-native e-batch-record providers are negotiating multi-asset master service agreements; microfluidic-hardware players are fielding requests for closed, GMP-ready pods that can be dropped into established manufacturing plants. In other words, tooling companies are no longer peripheral suppliers instead, they are fast becoming co-architects of the very platforms Big Pharma just paid billions to control. The winners will be those that can plug gaps today while designing modular solutions that won’t bottleneck the multi-indication pipelines these deals aim to unlock in the next five to ten years.

Three emerging CGT platform engines: in-vivo programmable cell therapy, systemic base editing and ex-vivo prime editing - ready to power a decade of multi-asset pipelines.

Strategic plays for tooling companies

To capture the white-space that Big Pharma’s platform buys have opened, CGT tool providers will need to stop thinking like commodity suppliers and start behaving like platform accelerators. The first step is commercial: price your offering against the value it unlocks across an entire multi-programme stack, not on a per-lot consumable basis. Next comes product architecture - design every module to plug seamlessly into either an in-vivo or ex-vivo workflow, because sponsors may soon straddle both. Data is the third pillar: milestone-heavy deals shift technical risk onto development partners, so the vendor that can surface lot-to-lot reproducibility, predictive release analytics and audit-ready batch records becomes indispensable. Finally, rethink deal structures altogether; in a world where the tool can determine whether dozens of assets reach the clinic, equity, royalties or shared IP could be worth more than a traditional supply contract.

Bottom line

Pipeline filler M&A is giving way to platform play M&A. For CGT tool providers, that means the next wave of growth will come from positioning your technology as critical infrastructure for these newly acquired operating systems. The winners will be those who can scale, standardise and data-enable the platforms that Big Pharma just paid billions to own.

Lonrú Lens will continue to track how these platform deals reshape the CGT value chain - and where enabling technology companies can capture value in 2026 and beyond.

The Non-Viral Delivery Surge: LNPs, Extracellular Vesicles & the Emerging Pipeline in Cell & Gene Therapy

What recent signals indicate

Each year, the American Society of Gene and Cell Therapy (ASGCT) annual meeting provides one of the clearest forward signals of where innovation is heading in CGT. With thousands of abstracts spanning academic, preclinical, and translational work, it acts as a near real-time readout of what platforms, targets, and tools are capturing attention and investment.

In April, we flagged a sharp uptick in lipid nanoparticle (LNP) interest across the 2025 abstract preview. Now, in the wake of Eli Lilly’s $1.3 B acquisition of Verve Therapeutics, that trend is no longer just academic. Verve’s GalNAc-functionalised LNP platform for in-vivo base editing offers a concrete signal that non-viral delivery is maturing into the clinic.

To be clear: many of these programs remain early-stage. It’s far from certain that in-vivo gene editing or exosome therapeutics will become the dominant modalities. But what’s emerging is a persistent and distinct trend line: away from viral vectors, and toward programmable, scalable, and re-doseable delivery platforms.

This post offers a tactical recap, from the data to the deals, and highlights what CGT tech providers should be doing now to stay ahead.

What’s Emerging? Key Technical Trends

From in-vivo CAR-T therapies to prenatal gene editing and designer extracellular vesicles, the technical conversation is evolving fast. This year’s standout sessions point to a distinct pivot: CGT developers are increasingly pursuing delivery systems that are programmable, re-doseable, and capable of bypassing traditional manufacturing bottlenecks. Each modality has different CMC and clinical implications, but all push the field closer to de-centralized, patient-centric models.

In-vivo CAR-T via targeted LNPs

Bypasses costly and logistically complex ex-vivo manufacturing and enables re-dosing potential.

Talk highlight: “Cell-targeted LNP‑based CAR‑T Therapy for B‑cell Malignancies”Prenatal gene editing using LNPs

Uses LNPs to treat congenital disease in utero, pushing boundaries of delivery and ethics.

Talk highlight: “LNP‑Based Delivery Systems for Prenatal Applications & Ethical Considerations”Designer extracellular vesicles (EVs)

Natural bio-distribution with tunable tropism; lower immunogenicity profile than synthetic carriers.

Talk highlight: “Scalable Manufacturing of MSC‑Derived EVs for Oncology”

Figure 1 | From syringe to hepatocyte in one step.

A single intravenous dose of ionizable-lipid nanoparticles (LNPs) delivers base-editing RNA directly to the liver, bypassing ex-vivo manipulation and shortening the therapeutic chain to needle-to-target.

Real-World Momentum via Deal Flow

Non-viral delivery platforms are no longer just for fringe programs. In the month following ASGCT, major deals and facility announcements like Lilly’s $1.3B buyout of Verve and BASF’s new excipient hub, reinforce the commercial weight behind this trend. From big pharma acquisitions to upstream investment in GMP infrastructure, the ecosystem is visibly recalibrating to support non-viral modalities.

Tactics for Enabling Technology Providers

For tech providers in analytics, mixing, excipients, or cleanroom design, the message is clear: adapt now to serve the next generation of therapies. Tactical moves like securing GMP lipids, modularizing mixing systems, or redesigning lipid analytics aren’t speculative, they’re prerequisites for relevance. Lonrú’s VantagePoint dashboards help prioritize what matters by product class and market stage.

How Lonrú Consulting Can Help

Lonrú helps enabling tech companies make strategic sense of CGT market shifts. Whether you're refining your value proposition, identifying high-fit partners, or plotting entry into the non-viral delivery space, we deliver clarity and actionability. Our approach blends market intelligence with customized partner strategy and commercial mapping ensuring you don't just track trends, you lead them.

Strategy Depth: We don’t just summarize the buzz, we decode its strategic consequences. Our VantagePoint™ Insights platform helps you see around corners.

Execution Alignment: Whether you’re building out your product roadmap or targeting new customers, we offer partner-mapping and strategy to align growth with opportunity.

Non‑Viral Commercial Strategy: If your technology enables non-viral therapeutic developers, we can help you map your market, position your offering, and sharpen your go-to-market plan.

Bookmark earlier reads

Through the Lonrú Lens - What to Watch at ASGCT 2025 (May 2025) for our conference preview that first spotlighted the looming LNP surge and non-viral delivery sessions.

From Bottleneck to Backbone: Building the U.S. ‘Interventional-Genetics Interstate’ (June 2025) for a deep dive into modular GMP build-outs, micro-batch production, and the equipment choices enabling rapid scale-up.

Meeting on the Med: A Pulse Check on CGT (April 2025) for field notes on industrialization pressures, COGs calculations and the analytics upgrades vendors must make to stay competitive.

From Bottleneck to Backbone: Building the U.S. “Interventional-Genetics Interstate”

Pioneer of next-generation gene editing, David Liu’s challenge at last week’s FDA cell and gene therapy round-table was stark: if the United States can compress concept-to-clinic manufacturing to “well under 90 days,” at least a thousand ultra-rare patients could receive bespoke in-vivo gene-editing therapies by 2030. The underlying science may be ready, but the physical and digital scaffolding that would let those therapies flow is not. Below is a high level review of where the U.S.’s infrastructure currently stands, where the cracks lie, and how proven international models can help finish the road in time.

A patchwork that almost works

Start-ups and academics have shown glimpses of what an agile infrastructure might look like. Philadelphia’s CHOP/UPenn Clinical Vector Core has produced 181 GMP vectors for 37 INDs touching 859 patients since 2007, showing what lean, mission-driven facilities can do over time. Vector production timelines remain a bottleneck for the field - Andelyn Biosciences’ 16-suite Columbus headquarters released its first clinical AAV lot in May 2025 ten months after tech-transfer began. Other modalities are emerging to address the shortcomings of vectors - in Boston, Landmark Bio’s 44 k ft² “full-spectrum” facility producing mRNA, LNPs and traditional vector products has been running since late 2022, providing eight re-configurable cleanrooms within walking distance of the Harvard–MIT medical cluster. Federally, the Bespoke Gene Therapy Consortium (BGTC) selected eight prototype diseases in May 2023 to demonstrate a repeatable regulatory-and-manufacturing playbook, while NINDS’ URGenT Network continues to fund IND-enabling work for ultra-rare neurologic disorders under its January 2025 funding notice (PAR-25-326).

Yet capacity is brittle. National Resilience, once the poster-child for “mega-factory” gene-therapy CDMOs announced yesterday, that it will close six of its ten U.S. sites because “capacity expansion has outpaced demand”. The message is clear: square footage alone does not guarantee throughput.

The gap between ambition and reality

Even with bright spots, most sponsors still wait nine months or more for GMP vector slots, rely on site-specific QC assays, and repeat pre-clinical toxicology from scratch; miles away from Liu’s sub-90-day aspiration. The United States currently lacks:

Geographic reach. Production remains concentrated in a handful of coastal hubs; patients elsewhere often cross state lines for dosing.

Shared digital infrastructure. Batch-release data live in siloed LIMS, making cross-site comparability almost impossible.

Economic resilience. Large plants built for blockbuster demand now sit idle, while hospital vector cores cannot scale beyond a dozen lots per year.

Lessons from health systems that are already doing it

The U.K.’s Advanced Therapy Treatment Centre (ATTC) Network embeds GMP suites inside NHS hospitals and links them through a national digital backbone. In February 2025 the UK government injected another £17.9 million to extend the model, explicitly to accelerate early-phase ATMP trials across the country. Every centre runs 2–4 multipurpose rooms and shares a harmonised set of SOPs - exactly the federated approach Liu argues the U.S. needs.

Singapore’s ACTRIS hub takes the same idea to city-state scale: 14 GMP-compatible suites, four translational labs and a single QC core feed hospitals, academics and start-ups under one roof, coordinated by a government logistics task-force. Both systems show that small, interoperable nodes can beat single mega-sites on utilisation, workforce agility and patient proximity.

Investing in nimble, connected manufacturing infrastructure today paves an Interventional-Genetics Interstate that will shorten timelines, cut costs and most importantly get transformative treatments to rare-disease patients faster.

How a U.S. Interventional-Genetics Interstate could take shape

Repurpose idle space. One wing of a downsized Resilience plant could house several 500 ft² closed-system pods tailored to micro-batch gene-editing runs, while the rest converts to warehousing and analytics. That keeps sunk capital alive without overshooting local demand.

Create a national QC cloud. Require BGTC and URGenT awardees to deposit release data into a shared LIMS opening the door to “plug-in” manufacturing sites that regulators can audit remotely.

Adopt a “grants-not-guarantees” funding model. NIH C06 facility grants and state matching schemes already release construction dollars in tranches tied to occupancy or throughput milestones; the same approach could seed regional micro-factories without repeating past oversupply.

Spin a workforce fly-wheel. Short, NIIMBL-style bootcamps that rotate technicians between hospital cores, CDMOs and start-ups would create a steady talent circuit instead of one-off hiring sprees.

Institutionalise digital twins. Inline PAT sensors plus cloud process models now routine in UK Catapult pilots, can cut tech-transfer time and give the FDA live visibility, shaving weeks off each bespoke batch.

What it means for technology suppliers

For analytics and PAT vendors, interoperability will clinch procurement decisions. Equipment makers should design skids that fit tight footprints and swap quickly between AAV, LNP and mRNA workflows. Digital-platform providers can own the value chain by stitching together batch genealogy from lab bench to hospital bedside. In short: if your tools make micro-batch production faster, cheaper and easier to regulate, the Interstate will need you.

The road ahead

The United States already has all the raw materials: pioneering science, ambitious CDMOs, and a small but growing federal appetite for public-private gene-therapy ventures. What it lacks is connective tissue. The next five years will decide whether the U.S. can deliver a federated, nimble network that can crank out micro-batches for 7,000+ ultra-rare conditions. Borrowing the ATTC formula of regional hubs plus national standards, and the ACTRIS emphasis on co-located clinical-manufacturing ecosystems, could close today’s fissures faster than any single plant investment. The prize is tangible: a future in which a child diagnosed this morning could receive a customised in-vivo therapy before the end of the school term.

Reflections from ASGCT 2025

He Wishes for the Cloths of Heaven

W. B. Yeats (first published 1899)

Had I the heavens’ embroidered cloths,

Enwrought with golden and silver light,

The blue and the dim and the dark cloths

Of night and light and the half-light,

I would spread the cloths under your feet:

But I, being poor, have only my dreams;

I have spread my dreams under your feet;

Tread softly because you tread on my dreams.

A breakthrough worth noting: an n-of-1 gene-editing therapy. Let’s celebrate the science, but keep patients and their families front-of-mind and proceed with care as we work to reform the business model.

On the flight home from New Orleans, the week’s jazz still echoing in my earbuds, a line from Yeats surfaced -“Tread softly because you tread on my dreams.” It summed up my reflection on the hopes and uncertainties that patients and families carry as they wait for the promise of cell and gene therapies.

A milestone worth celebrating

Professor Kiran Musunuru’s late-breaking CPS1 “N-of-1” base-editing success in baby KJ created much excitement and celebration. Six months from molecular diagnosis to first infusion; ammonia crises averted; a liver-transplant listing cancelled. As blueprints for bespoke in-vivo editing go, this one is pure architectural poetry.

Yet one swallow does not make a summer

Our modelling estimates, visible here pulling on published commercial GT COGs and the three-dose LNP regimen puts the price tag for this breakthrough therapy well north of US $1 million. Even if payers were willing, the bespoke CMC, analytics and logistics cannot be amortised across a wider patient pool today. KJ’s story is a beacon, not yet a bridge.

Voices that kept us grounded

In a powerful fireside panel, patient-advocate Oralea Marquardt reminded us what happens when hopes are shattered after investors pivot and trials are shelved. Prof. Don Kohn recounted how an approved ADA-SCID gene therapy survived only by shifting into a Public Benefit Corporation (Rarity Inc.) when Orchard exited. Dr Claire Booth urged proportionate regulation and innovative reimbursement, warning that repeated withdrawals erode family trust.

Their refrain? Language matters. So does honesty about timelines, affordability, and the probability that your child may not make the inclusion cut.

The industry’s unrequited love story

Capital may flow to platforms that promise scale, not to ultra-rare programmes that demonstrably save lives but defy spreadsheet logic. Until we align payment models and regulatory pathways with clinical value delivered, scientific breakthroughs will continue to outrun commercial reality. Musunuru himself flagged the need for shared reagent banks and harmonised analytics to lower entry costs for single-patient INDs.

Where Lonrú sees light

Platform-ready modular CMC dossiers - codify repeatable elements so every next bespoke therapy starts at 60 % completion.

Outcome-based annuity payments - spread the >$1 M sticker over durability, with claw-backs for under-performance.

Public-interest manufacturing co-ops - echoing Rarity’s public benefit corporation, pool idle academic clean-room capacity for ultra-rare runs.

Digital evidence commons - capture long-term real-world data to sharpen cost-effectiveness arguments and feed adaptive pricing.

Treading softly, but moving forward

Yeats’ plea is our directive: each dataset, each funding decision, each splashy headline lands on someone’s dream. Let’s celebrate KJ’s reprieve without overselling affordability and timelines for every rare disease. Let’s channel the excitement into structural fixes that let breakthrough science and sustainable business models grow in tandem.

At Lonrú, illuminating that path, from innovation to equitable impact is our raison d’être. We invite partners who share this conviction to walk with us, softly but determinedly.

- written by Lonrú Consulting’s Principal and Founder, Caoimhe Nic An tSaoir, PhD MBA

Illuminate your next step. Reach out to explore Lonrú’s VantagePoint™ frameworks.

How patient-led business models are accelerating the next wave of cell & gene therapies

This week’s ASGCT kicked off with a half-day workshop that put patient advocacy organisations (PAOs) centre-stage: “The Business of Advocates Advancing CGTs.” The line-up showcased six distinct financing and operating models that rare-disease groups are already using to push novel therapies from idea-to-IND and, in a few cases, to market.

Why does Lonrú care? Because every one of these blueprints re-writes the traditional value chain, creating new touch-points where enabling-technology providers can plug in and add velocity. Below is our take on what’s working, where the white-space lies, and how the field can move faster—together.

1. Venture Philanthropy: recycling capital, de-risking pipelines

PAOs such as EB Research Partnership have proven you can pair philanthropy with an equity stake and then redeploy the upside into the next programme. Capital recycling has already generated multi-billion-dollar returns in cystic fibrosis and is now fuelling gene-therapy approvals.

Lonrú lens: This model needs sharp diligence on equity, royalty waterfalls and post-marketing obligations—areas where our VantagePoint™ Scale framework routinely stress-tests cash-flow projections and pricing scenarios.

2. “Virtual Biotech” & Parent-Run INDs: lean, data-rich, execution-focused

FOXG1 and Cure Rare Disease keep IP and the IND inside the foundation, while outsourcing CMC and clinical operations. With <$10 million they can marshal CROs, CDMOs and AI-assisted registries to reach first-in-human trials.

Lonrú lens: An AI-enabled, gap-analysis tool can shave months off regulatory prep and keep lean teams focused on go/no-go inflection points.

3. Social-Purpose Corporations (SPCs): mission lock with investment flexibility

Elpida Therapeutics channels philanthropic and venture dollars into a public-benefit corp, ring-fencing mission while still courting mainstream capital.

Lonrú lens: Governance complexity is real, but SPCs open a route for ESG-oriented investors looking for measurable patient impact alongside returns—a sweet spot for differentiated analytics and storytelling.

4. Hospital-Held Licences: academic GMP meets cost-recovery access

Great Ormond Street is preparing to license and manufacture an ADA-SCID therapy abandoned by industry, aiming for cost-price delivery within the NHS.

Lonrú lens: When sponsors exit, institution-led rescue pathways preserve clinical know-how and datasets. They also create demand for modular QC, batch-release and real-world-evidence solutions that technology vendors can supply at scale.

5. Capacity-Building Grants (CZI Rare-as-One, PCORI): seeding data infrastructure

Five-year grants of up to $2 million are giving fledgling groups governance training, registry tooling and DEI mandates that de-risk later venture rounds.

Lonrú lens: Data is the currency. Offering in-kind AI analytics or registry architecture can be a strategic “give-to-get” for service providers aiming to become embedded long before commercial inflection.

6. Event- & Media-Driven Revenues: community engagement that pays for R&D

From $10 million reality-show prizes to cross-country endurance events, creative fundraising is underwriting natural-history studies and AAV vector work.

Lonrú lens: Volatile by nature, but high-visibility campaigns drive brand equity and patient-reported outcomes—alongside rich datasets that feed development models.

Where patient advocacy becomes the catalyst for next-gen cell & gene therapies.

Three strategic signals for the road ahead

Capital efficiency matters more than capital volume. Each archetype hinges on agile, data-guided decision gates—exactly where AI-powered market and regulatory intelligence can compress timelines and costs.

Ownership of IND-critical data is becoming the bargaining chip. Whether a PAO holds equity, an SPC licence, or a hospital marketing authorisation, control of natural-history and CMC datasets dictates partnering leverage.

Ecosystem players that illuminate complexity will win. The most successful advocates are not just funding experiments; they’re curating information—registries, biobanks, outcome measures—now ripe for advanced analytics and digital-first collaboration.

Where Lonrú Fits

Our mission is to accelerate growth for the technologies that enable CGT breakthroughs. The alternative models highlighted at ASGCT open multiple entry points for our clients:

VantagePoint™ Insights to benchmark emerging PAO pipelines against partner demand.

VantagePoint™ Validation to design capital-efficient tech-transfer and CMC roadmaps that suit lean, virtual structures.

VantagePoint™ Connect to matchmake between mission-driven funds, hospital GMP suites and enabling-tech innovators.

Illuminating the route from patient-driven discovery to scalable market success.

Ready to illuminate your next move? Let’s talk at ASGCT in New Orleans—or book a virtual debrief post-meeting.

Through the Lonrú Lens – What to Watch at ASGCT 2025

The American Society of Gene & Cell Therapy’s annual meeting is always a bell-wether for where the field is heading, and this year’s New Orleans programme is the biggest yet. Our data-driven sweep of the abstracts surface five story-lines worth tracking – plus a free interactive dashboard to help you cut through the noise once you arrive in NOLA.

1. 2,196 reasons to plan your diary

2,196 presentations spread over five days – workshops, orals, symposia, posters and fireside chats.

1,925 individual speakers from 1,094 organisations.

Poster-heavy: ~67 % of all slots.

Take-away → the sheer scale demands a smart filtering strategy.

2. AAV still wears the crown – but the court is changing

Below is a quick-glance infographic of the five strongest themes surging through the agenda:

General gene therapy & AAV delivery remains the heavyweight, anchoring ≈ 640 talks that probe tropism, PK/PD and clinical translation.

CAR-T and other engineered T-cells follow with just over 320 sessions, reflecting the field’s pivot toward solid-tumour applications and off-the-shelf platforms.

AAV production & manufacturing clocks in at ≈ 250 presentations, proof that CMC and scale-up have moved from backstage to centre stage.

LNP–mRNA delivery—once a niche—now commands nearly 90 slots, signalling non-viral vectors’ mainstream arrival.

And AAV capsid engineering for CNS rounds out the leaderboard with ≈ 80 talks, underscoring the race to breach the blood-brain barrier.

Talk Hotspots: Top 5 Topics at ASGCT 2025

3. Gene editing graduates from “emerging” to essential

Editing-related abstracts almost double year-on-year (122 talks). While Cas9 platform work still leads, prime/base editing, compact nucleases and first-in-human in-vivo data are pushing the field from tool-building towards translation.

4. Who’s punching above their weight?

Academia still owns the podium – UMass Chan, Duke, Minnesota, Fred Hutch – yet tool suppliers such as Thermo Fisher and Millipore Sigma climb the rankings with manufacturing and analytics content. Corporate voices are broad but not yet dominant: the top-20 companies represent <15 % of the agenda.

5. What narratives will shape corridor talk?

Below is a visual snapshot of the four “big-picture” narratives we believe will dominate the hallway chatter in New Orleans. Use it as a quick mental map, then scroll on for the deeper dive in our interactive tool.

Manufacturing Moves Mainstream – nearly 250 abstracts tackle capacity, process intensification and analytics, reflecting the sector’s new clinical bottleneck.

Delivery Diversification – with ~90 LNP-mRNA talks and 80+ capsid-CNS sessions, non-viral and next-gen viral vectors are hedging against single-platform limits.

Precision Editing Surges – the fastest-growing cluster at 120+ presentations, spanning prime/base editors, compact nucleases and first-in-human data.

Oncology Evolves – more than 320 engineered-cell abstracts showcase armoured/allo CAR-Ts, NK and macrophage approaches pushing beyond haematologic malignancies.

Together, they frame the strategic questions investors and BD teams will be asking long after the plenaries end.

Four Trends Shaping ASGCT 2025

Meet us on-site & try our free scheduling tool

Our founder, Dr Caoimhe Nic An tSaoir, will be on the ground all week – connect with her to discuss how Lonrú’s data-first approach can illuminate your business decisions.

To make those decisions easier, we’re sharing a complimentary interactive dashboard:

Search the entire programme by topic cluster, speaker or organisation.

Visualise busy time-blocks to avoid clashes.

Zero in on your niche – whether it’s capsid engineering, LNP formulation or clinical trial design.

It’s the fastest way to find your “must-see” talks amid 2k+ abstracts – and it’s yours, free, courtesy of Lonrú.

👉 Try the dashboard below and bookmark it before you pack your bags.

Why talk to Lonrú?

If you’re an enabling-technology or tools company, our VantagePoint™ suite turns noise into strategic clarity: market intelligence, validation road-maps, go-to-market acceleration and investor engagement – all backed by AI/ML analytics. Let’s discuss how we can help you stand out long after the convention centre lights dim.

Meeting on the Med: a pulse check on CGT

The Alliance for Regenerative Medicine’s Meeting on the Med brought therapeutic developers, regulators, investors, manufacturers and technology vendors together for three intense days of debate and deal‑making in Rome. From main‑stage keynotes by EMA Executive Director Emer Cooke to packed break‑outs on automation and payment models, the conference offered a clear signal: 2025 is the year CGT moves from pilot phase to industrial scale.

Below are five high‑level themes that dominated the agenda, paired with practical ways Lonrú Consulting can help stakeholders translate talk into traction.

Dr Caoimhe Nic An tSaoir, PhD MBA representing Lonrú Consulting at its first ARM Meeting on the Med—illuminating innovation in Rome.

Industrialisation & Cost‑of‑Goods: from artisan to assembly line

Conference focus

Speakers from Cellares, ScaleReady and SmartCella touted up to 10× productivity gains with closed, automated systems, while plenary panels urged “robotics, AI and digitalisation” to improve labour hours.

Why timing matters – Conference veterans warned: “Don’t bolt robots onto a sub-optimal process.” The smart sequence is:

Close & automate the core workflow to drive consistency.

Iterate and optimise based on fresh, high-fidelity data.

Roboticise only when the process is lean enough to justify the CapEx.

Where Lonrú helps

VantagePoint™ Scale models the true economics of automated vs. manual workflows—integrating batch size, labour inputs and capital depreciation—so equipment vendors and therapy developers can make evidence‑based CapEx decisions.

2. Regulatory Convergence: alignment gives way to harmonisation

Conference focus

EMA, MHRA, AIFA and other agencies previewed a joint dossier framework for ATMPs, signalling a shift from bilateral “alignment” to multilateral convergence in 2025‑26. Under this model, one core CMC/clinical package could be reviewed simultaneously by several regulators, trimming duplicate studies and bringing therapies to multiple markets months sooner.

Where Lonrú helps

VantagePoint™ Insights offers a policy tracker that maps emerging common modules, review timelines and regional inflection dates —allowing CGT technology suppliers to support submissions and market launches with confidence.

3. Financing Climate: capital comes with a data‑driven thesis

Conference focus

Investors are showing signs of optimism that deal flow will rebound in H2 2025, but before cheques are written they want proof of differentiated tech, clear ROI and capital‑efficient scale‑up paths. Capital will flow first to platforms able to quantify near-term revenue and manufacturing economics.

Where Lonrú helps

VantagePoint™ Accelerate packages market sizing, NPV/DCF modelling and competitive white‑space analysis into investor‑ready narratives—helping technology providers translate ground-breaking science into a thoroughly de‑risked business case.

4. Ethics, Access & Novel Payment Models: transparency is non‑negotiable

Conference focus

Panels on ethics urged more openness around cost of goods, while payers showcased staged‑payment and subscription pilots to manage six‑figure therapy costs. A shared takeaway emerged: sustained access depends on communicating with transparency and demonstrating tangible value—tailored to regulators, payers, clinicians, and patient communities alike.

Where Lonrú helps

VantagePoint™ Illuminate distils complex value propositions and pricing strategies into clear, stakeholder‑specific messaging—supporting technology firms as they negotiate value‑based contracts and build public trust.

5. Emerging Geographies: the Gulf states step onto the CGT stage

Conference focus

A dedicated session spotlighted UAE and KSA initiatives to build GMP capacity and local innovation hubs, with regional investors actively scouting technology partners. Speakers emphasised the opportunity; whoever locks in early reference sites now will shape standards for a market that is forecast to treat tens of thousands of regional patients by 2030.

Where Lonrú helps

VantagePoint™ Connect maps innovation clusters, stakeholder networks and funding programmes in any target geography, then brokers introductions for enabling-technology providers to regulators, hospital networks, strategic investors and channel partners—giving first movers the inside track on commercial pilots and policy dialogues.

The takeaway

The ARM meeting in Rome confirmed that scale, regulatory convergence, and credible economics are now the gating factors for progress in CGT—and it is the enabling-technology companies who can unlock every one of those gates. Lonrú’s mission to Accelerate Growth of Cell and Gene Therapy Technology Companies — exists precisely to drive momentum at this inflection point.

Whether you’re rolling out an automated manufacturing platform, launching next-gen analytical tooling, or scaling a digital batch-record system, Lonrú turns fresh industry insights into practical roadmaps—combining market intelligence, stakeholder alignment, and financial modelling so breakthrough technologies reach industrial impact sooner. Ready to view your CGT strategy from a higher vantage point? Let’s talk.

Unlocking Cell and Gene Therapies: Introducing VantagePoint™ – Lonrú Consulting’s Suite of Solutions For Growth

As cell and gene therapies (CGT) continue to revolutionize medicine, enabling technology companies are increasingly becoming a key pillar of progress. These companies develop critical platforms, tools, and technologies that facilitate the scalable, cost-effective, and precise production and delivery of groundbreaking treatments. At Lonrú Consulting, we understand that these enabling technologies are more than just support systems—they form part of the vital infrastructure required to democratize access to advanced therapies globally.

That’s why we’ve developed VantagePoint™, a comprehensive suite of solutions carefully crafted to propel enabling technology companies at every stage of their growth journey. VantagePoint™ encapsulates our deep industry expertise and advanced AI-driven analytics into a unified approach, uniquely positioning our clients to overcome challenges, identify opportunities, and accelerate commercialization within the dynamic CGT landscape.

Lonrú Consulting’s VantagePoint™: A Unified Suite of AI-powered Solutions Propelling Enabling Technology Companies at Every Stage of Growth.

The VantagePoint™ Advantage

VantagePoint™ addresses the fundamental areas critical to the growth and scalability of enabling technology providers:

VantagePoint™ Insights – Strategic market intelligence that provides real-time, actionable clarity, empowering your company to anticipate market trends, understand competitive landscapes, and make confident, informed decisions.

VantagePoint™ Validation – Strategic technology validation and partnering solutions, helping emerging technology providers navigate complexity with confidence, secure robust partnerships, and validate innovations strategically within the competitive CGT market.

VantagePoint™ Accelerate – Precision-driven go-to-market and business development strategies designed to fast-track commercialization, optimize financial planning, and accelerate market adoption, ensuring that innovative technologies reach the patients who need them, faster.

VantagePoint™ Illuminate – Tailored strategic positioning and messaging that clearly articulates your technology’s unique value, enhancing brand visibility, and effectively engaging stakeholders, from investors to industry partners.

VantagePoint™ Connect – Strategic stakeholder engagement services, leveraging deep market connections and relationship-building frameworks to align enabling technology companies with key translational networks, biotech firms, investors, patient advocates and industry leaders for impactful collaboration and accelerated growth.

VantagePoint™ Scale – Comprehensive commercial feasibility and strategic scaling support, delivering robust pricing strategies, detailed market entry roadmaps, and scalable growth frameworks that ensure sustainable, long-term commercial success.

Enabling Technologies: The Key to Democratizing Advanced Therapies

By optimizing the reach and placement of innovative enabling technologies, Lonrú Consulting helps to democratize the transformative potential of cell and gene therapies. These technologies significantly reduce costs, improve accessibility, and enhance treatment precision, ultimately allowing more patients across diverse geographic and economic contexts to benefit from cutting-edge treatments.

Lonrú Consulting: Your Partner in Transforming CGT

Lonrú Consulting was founded on the vision of illuminating opportunities within the CGT industry. With over 15 years of global experience in the life sciences sector, Lonrú Consulting, led by Dr. Caoimhe Nic An tSaoir, integrates scientific rigor with strategic acumen, uniquely positioning us to support enabling technology companies effectively.

We have specifically tailored our expertise to empower technology providers, understanding that their success directly translates into broader patient access to life-changing therapies. Through VantagePoint™, we provide clarity, strategic insight, and precise execution, driving your company's success while catalyzing the industry’s evolution.

At Lonrú, we believe the future of cell and gene therapy depends heavily on innovation in enabling technologies. Together, let’s illuminate the route to viable transformative therapies.

Let us illuminate your business—contact us to discover how the VantagePoint™ suite can accelerate your journey in cell and gene therapy.

Navigating Strategic Partnerships: How Platform Technology Providers Can Overcome Validation Challenges

At last week's Advanced Therapies UK meeting, one theme resonated clearly among platform technology companies supporting cell and gene therapy (CGT) production: the complex yet essential role of partnerships in validating their technologies. These strategic collaborations are critical, yet they often present significant hurdles, from scoping and initial engagement to execution.

Companies face multiple challenges when entering third-party partnerships. Firstly, the precise scoping of collaborations often proves difficult, leading to misaligned expectations and inefficient use of resources. Secondly, engaging suitable partners involves navigating complex negotiations and managing expectations around technology validation and intellectual property. Finally, executing these partnerships demands rigorous project management and clear, constant communication—areas where resource constraints frequently limit effectiveness.

Why are these partnerships vital? Successful validation through third-party collaborations provides crucial credibility, enhancing market trust and significantly boosting investor confidence. Moreover, strategic partnerships open doors to larger networks and new commercial opportunities, accelerating technology adoption and growth.

However, for many enabling technology companies, internal teams are deeply entrenched in R&D, fundraising efforts, or focused on sales execution and revenue generation, often leaving strategic partnership initiatives underserved. This is precisely where Lonrú Consulting steps in.

Launching Lonrú's VantagePoint™ Validation Platform: Illuminating strategic clarity for enabling technology companies in Cell & Gene Therapy.

At Lonrú, we specialize in illuminating critical strategic partnership needs. Our structured approach offers technology providers unparalleled visibility, strategic insight, and clarity when validating their enabling technologies. From clearly defined validation objectives and partner alignment to meticulous execution and impactful outcomes, our VantagePoint™ Validation platform ensures strategic clarity and precision in every partnership.

Explore more about our VantagePoint™ Validation platform and strategic partnership services here.

If you're an enabling technology company underpinning cell and gene therapy production or delivery, it's time to explore how strategic outsourcing can accelerate your journey. Let's illuminate your pathway to validation together.

Ready to discuss your strategic partnership needs? Connect with Lonrú Consulting today and let us help you turn your validation challenges into powerful opportunities.

Catalysing the COGs Revolution: The Role of Enabling Technologies in CGT

Lonrú is at Advanced Therapies UK this week and day one discussions highlighted emerging trends, groundbreaking innovations, and pressing challenges within the cell and gene therapy (CGT) landscape, placing a strong emphasis on enabling technologies and their critical role in addressing one of the industry's biggest hurdles—the Cost of Goods (COGs).

Enabling technology providers are emerging as key catalysts capable of significantly reducing COGs, addressing one of the industry's primary barriers to patient access. The keynote panel underscored how high manufacturing costs often prevent eligible patients from receiving approved therapies due to regional payer reluctance, emphasizing the urgent need for cost-effective solutions—precisely the type of innovation Lonrú champions.

A particularly compelling panel discussion, "Academic Translation: Advancing Cutting Edge Technologies," chaired by Lara Campana, from Resolution Therapeutics (a University of Edinburgh Spinout) delved deeper into the challenges faced by technology founders in establishing meaningful collaborations. When Lonrú posed the critical question, "Looking back, where do you see the biggest missed opportunities for enabling technologies or partnerships to accelerate development—and what would you do differently?" panelists candidly discussed the difficulties their teams encountered in demonstrating proof of concept of their technologies and managing complex industry collaborations, IP ownership, and partnership structuring.

These insights resonate strongly with Lonrú's expertise. We specialize in identifying, cultivating, and establishing strategic collaborations, effectively bridging the gap between academic innovation and commercial execution. Our tailored approach and advanced analytics help enabling technology providers navigate complexities, optimize commercialization pathways, and significantly lower COGs.

As the industry progresses, the imperative is clear: innovation must be paired with strategic partnerships to achieve tangible cost reductions and improve patient accessibility worldwide.

If you're ready to leverage your enabling technology for maximum impact, Lonrú is here to illuminate your path forward.

Illuminating CRISPR Clinical Trial Progress: A Lonrú Lens for Enabling Tools Providers

A recent Keystone meeting showcased a multitude of CRISPR-based clinical trials, underscoring the tremendous growth and development in the field. As excitement around CRISPR therapies intensifies, enabling tools providers—ranging from assay developers to manufacturing technology companies—are uniquely positioned to support these therapeutic programs in critical ways. In this post, we take a close look at some of the latest CRISPR clinical trial updates (therapeutic applications only) and introduce Lonrú Consulting’s new public dashboard designed to help enabling technology companies recognise emerging needs and opportunities.

CRISPR Therapeutics: What’s New from Keystone?

This year’s Precision Genome Engineering Keystone meeting confirmed that CRISPR-based therapies have made considerable strides, with an approved therapy now commercially launched and an expanded pool of proof-of-concept data and early clinical safety readouts for new indications. Key highlights include:

Emerging Pipeline Diversity

While oncology and monogenic hematological diseases continue to account for the majority of CRISPR clinical trials, diversity of clinical trial categories is expanding to include neurological disorders and metabolic diseases.

This broadening pipeline hints at a growing need for specialized vectors, delivery systems, and lab instrumentation that can facilitate gene editing across a wider range of cell types and patient populations.

Focus on Delivery and Efficiency

Many panels spotlighted the importance of refining both ex vivo and in vivo delivery modalities. This shift underscores the demand for robust viral and non-viral delivery tools, high-fidelity nucleases, and scalable manufacturing platforms—all areas where enabling technology providers can shine.

Quality and Regulatory Considerations

As CRISPR programs move through clinical phases, compliance with evolving global regulatory standards has become paramount. Tool providers offering GMP-ready reagents, automated QC processes, and validated assay kits stand to gain traction as sponsors seek to streamline their clinical workflows from pre-clinical development to clinical manufacture.

Why It Matters for Enabling Tools Providers

CRISPR sponsors rely on high-performance instrumentation, reagents, software, and manufacturing technologies to maintain clinical momentum. From single-cell analysis platforms that verify gene edits to advanced vector packaging systems, every stage of CRISPR therapy development demands specialized support.

Assay & Analytics

Tool developers can build or adapt products that precisely predict or measure gene-editing efficiency, off-target effects, and cell viability. Demand continues to grow for analytical solutions that can scale from early R&D to late-phase GMP settings.Automation & Scale-Up

As more candidates progress into mid- and late-stage trials, sponsors will need integrated, automated workflows—particularly for ex vivo engineering of immune cells and beyond. Vendors who provide modular, automated solutions can help sponsors reduce costs and improve reproducibility.Regulatory-Grade Toolkits

Enhanced guidelines around gene editing are emerging. GMP-certified reagents, standardized protocols, and robust documentation platforms offer sponsors peace of mind and help expedite regulatory approvals.

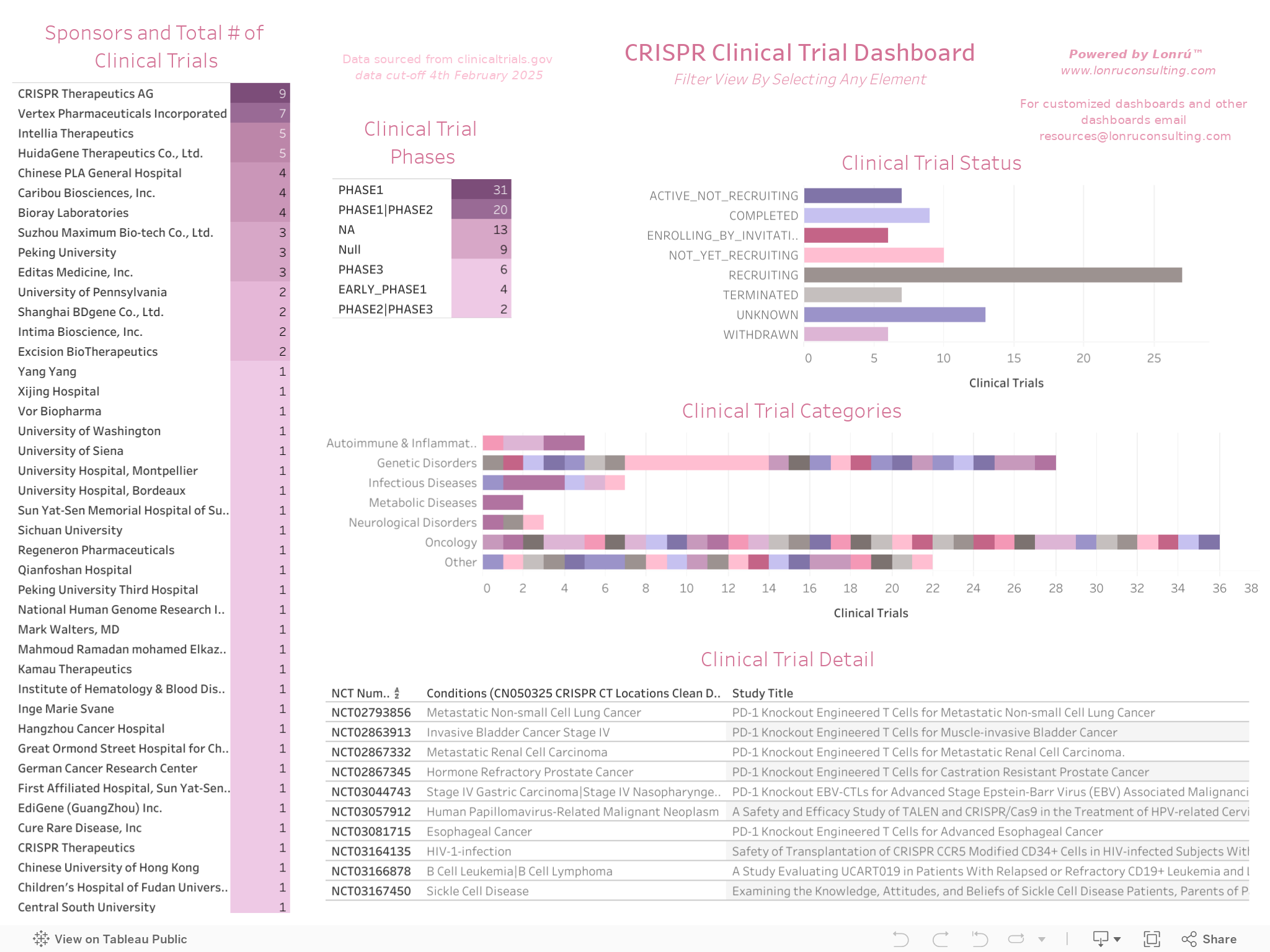

Introducing Lonrú’s CRISPR Clinical Trial Dashboard

In line with our mission to help technology providers identify strategic opportunities, Lonrú Consulting is releasing our new, publicly accessible CRISPR Clinical Trial Dashboard below and on our interactive dashboards page. This interactive database lets you:

Browse Active Sponsors and Investigational Targets

Instantly see which companies are leading in oncology, rare diseases, or other emerging applications—to map those areas back to their specialized tool needs.Filter by Phase, Status, and Indication

Determine where your tools and technologies can fit best based on trial phase (e.g., early-phase for novel assays vs. near-market for scalable manufacturing solutions).Pinpoint Potential Partnerships

Identify top CRISPR sponsors that may be seeking next-gen delivery methods, automation solutions, or advanced analytics to complement their therapeutic pipelines.

By consolidating and visualizing information on CRISPR therapeutic trials, we aim to give enabling tools providers an easy way to track potential leads, time new product launches, and tailor their solutions to fast-evolving sponsor needs.

How Enabling Tools Providers Can Use Lonrú’s Dashboards

Market Positioning

Understand which clinical areas (e.g., B-cell malignancies, sickle cell disease) are seeing the greatest CRISPR activity, and tailor your product roadmap or marketing accordingly.

Targeted Business Development

Pinpoint sponsors that match your capabilities—whether you offer reagents optimized for allogeneic cell therapies or automation equipment ideal for large-scale gene editing.

Competitive Benchmarking

Track your peers (other platform and tool vendors) to see how they are positioning their products across varying therapeutic trials. Use these insights to refine your messaging or to guide strategic investments in R&D.

Regulatory & Compliance Insights

Monitor how trials across different geographies progress through regulatory milestones. Align your quality management systems and documentation practices to meet sponsor expectations in each region.

Closing Reflections

Keystone illuminated just how quickly CRISPR therapeutics are evolving. For enabling tools providers, each new clinical milestone signals a rising need for more specialized, reliable, and scalable products. With sponsors juggling multiple priorities—speed, safety, cost efficiency, and regulatory compliance—there’s never been a better time to cement your role as a crucial partner in the CRISPR value chain.

Lonrú Consulting invites you to explore our dashboard and harness these data-driven insights. If you’d like to learn more about how we can help you position your technologies or amplify your market impact, we’re here to illuminate the path forward.

Ready to dive in?

Customize our CRISPR Clinical Trial Dashboard to uncover key trends and potential partnerships. Reach out at info@lonruconsulting.com or visit Lonrú Consulting to learn how our data analytics and strategic advisory can illuminate your next big opportunity.

At Lonrú Consulting, we believe in empowering the technologies behind the therapies. Together, let’s unlock the full potential of CRISPR and continue shaping the future of genomic medicine.

Bridging the Gap—Enabling Technology Providers & the Path to the Clinic

Lonrú is attending the Precision Genome Engineering: Translating the Human Genome to the Clinic meeting in Killarney this week. The meeting brings together the leading minds in gene editing, delivery systems, and therapeutic development to discuss the latest advancements shaping the future of precision medicine. From new CRISPR-based tools and enabling technologies to the challenges of translating innovation into the clinic, the conference highlights the critical steps needed to move from discovery to impact. Our poster presentation yesterday on streamlining preclinical-to-IND pathways generated interest, not just from therapeutic developers, but also from enabling technology providers eager to gain a clearer view of the challenges their partners and customers face in clinical translation.

Why Are Enabling Technology Providers Paying Attention?

While much of the conversation around gene editing focuses on therapeutic breakthroughs, every successful CRISPR-based therapy depends on the enabling technologies that support it—from delivery systems and genome engineering platforms to advanced analytical tools and scalable manufacturing solutions. Many enabling technology providers recognize that to best serve their customers, they need a deeper understanding of:

✔ Regulatory bottlenecks that delay clinical progression and impact product adoption.

✔ Common reasons for IND holds, including safety concerns, CMC issues, and assay validation gaps.

✔ Preclinical validation requirements that define what data therapeutic developers need to move forward.

By better aligning their solutions with these pain points, enabling technology providers can position themselves as indispensable partners in the journey from discovery to the clinic.

Beyond the Poster: Full Report & Decision Trees

Attendees we met with appreciated having access to our full report to dive deeper into the topics covered in the poster. In particular, the decision tree framework resonated with both therapeutic and technology developers, offering a structured approach to mitigating risks early in the development process.